In this era of humongous growth and fast-paced development, startups and entrepreneurship have become a viable path for college students and youngsters, dreaming about revolutionising the world through their thoughts and actions. In order to materialise a viable idea into a full-fledged organisation, what we need is a persevering team, an adept analysis of the market segment, user traction and of course, funding.

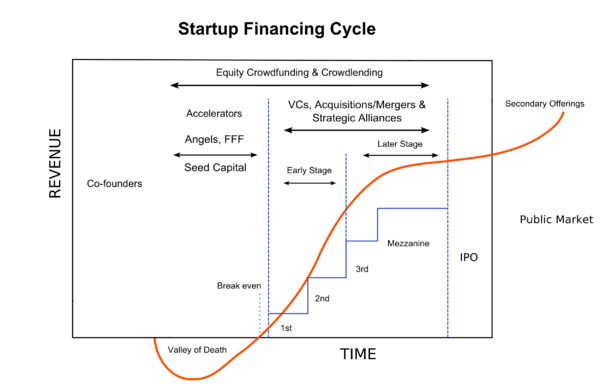

As you may have already deduced, procuring appropriate investments in the early stages of a particular startup seems to be a daunting task, and may also define your chances of proceeding into the further stages successfully. Every flourishing startup has to prevail over the “valley of death”, a position wherein the startup generates a negative revenue. That is when angel investors along with family and friends chip in with the seed funding, in order to tide over the valley of death.

Till the startups develop into full-blown listed companies, financial injections are required at different stages in order to satiate their high growth appetite and meet their working capital requirements.

Since the proliferation of the startup culture since the commencement of the millennium, various venture capitalists and private equity firms have also been conceptualized in order to provide instruments to invest in these high growth but equally high risky ventures.

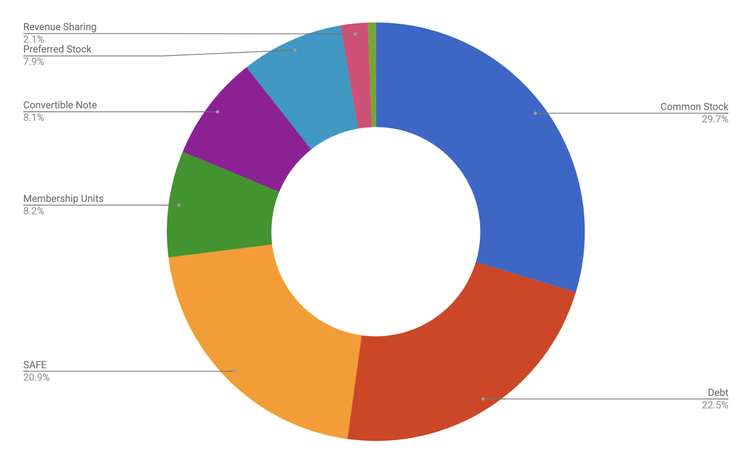

In the current situations, startups generally resort to either of three methods: the traditional priced equity round, convertible notes or the newly evolved SAFE notes. Each of the methods are bundled with pros and cons, and entrepreneurs frequently fail to adjudge the intricacies of each, which may lead to faulty valuation or low ownership and control over the firm.

Priced Equity Rounds

Conventional priced equity rounds are rarely utilised by a startup on the road for securing its first financing, since it involves deciding upon a pre-investment valuation (which cannot be approximated by established financial valuation techniques, since it’s too early to say) while also resolving the post-investment implications regarding the shareholder rights and the boardroom powers of the investors involved. These would not have worried the founders if the investors had settled for common stock, but venture capitalists generally go for preferred stock to maintain a stronghold in exchange for the exposure to the high risk. A below-par valuation cap may send out negative signals to the market regarding the firm, thus making it harder to garner funds in later financing stages, while an overvalued firm may not meet up to its expectations when the series funding rounds step in. Thus, equity rounds are generally adopted at later stages of startup financing when the founders have gained experience and the startup has been concretely valued.

Convertible Notes

Convertible notes have been the most trusted sources, as far as early stage financing is concerned, since it is a quicker and simpler mode of financing with lesser legal hassles involved.

Convertible notes are basically (loans), with the investments accruing a periodic interest till the next financing round or when a qualifying transaction underlined in the contract takes place, when the principal plus the interest is proportionately converted to equity. The maturity date mentioned in the contract is triggered only if no financing round occurs before the maturity date, in case of which the principal and the accumulated interest is returned to the investor.

As simple as it may sound, a few points of negotiation in the contract where the founders must act astutely are the interest rate and the amount of investment (principal). The intention of the investors and the founders may seem misaligned in this case, since in the later stages of financing, the founders may push for higher valuation (for obvious reasons, of course) while the investors are interested in lower valuations, since that results in higher number of shares for them and hence greater power over the firm.

In order to tackle this imminent contradiction, the convertible notes offer the facility of negotiating upon a valuation cap or a discount rate.

A valuation cap limits the share price offered to the early stage investors in the later equity financing round. For instance, if $1 Million is invested with a negotiated market cap of $10 million, and in the Series-A round (the first round of equity financing post-breakeven) the startup garners $20 Million with a pre-money valuation of $50 Million and a price of $10 per share, the share price for the convertible note holders would be $2 per share. The convertible note holders may also be offered a discount rate (generally between 10% and 30%) on the share price in the equity financing rounds. Most of the convertible note contracts have provisions to include both discount rates and valuation caps to cover the early stage risk taken up by the investors.

Convertible notes of course, come with an inherent risk of the startup being liquidated while paying out to the investors if the equity financing round is scheduled past the maturity date. The onus thus lies on the founders to negotiate on favourable terms while adjudging the financial situation.

Simple Agreement of Future Equity (SAFE)

SAFEs (or iSAFEs in the Indian concept developed by 100X.VC) have been recently developed to improve upon the shortcomings of the convertible notes and make the rounds of funding more friendly from the perspective of the founder.

The concept of the SAFE notes was introduced by Y Combinator in 2013, before 500Startups, another startup accelerator based in Silicon Valley introduced KISS (Keep It Simple Security) with a similar idea and plan of action. iSAFE was a phenomenal milestone in the Indian startup ecosystem by saving the trouble of going through a legal quagmire for novice founders. A 6-page agreement and the deal is done!

The most attractive part of the iSAFE deal is that no interest is charged on the investment, so it’s more like a warrant to convert to stocks at a later financing stage. The exit clause is a bit different from convertible notes’ in the sense that the investment is proportionately converted into equity at the first financing round after the investment (irrespective of the deal value).

The iSAFE contract also encompasses the provision of discount rate and valuation cap, and that’s where most founders may falter due to lack of experience. Most founders regard the valuation cap as the present valuation of the firm, which is definitely not the case since the value of the company cannot be calculated at such an early stage. Valuation cap relies more on prowess in negotiation rather than on mathematics, and thus the ball is in the founders’ court.

The major fallacy which the founders fail to notice while incessantly signing iSAFE deals is the real dilution percentage once the iSAFE is triggered and the investment materialises into shares, since most of the founders do not maintain a dynamic cap table. It thus becomes really important to track each and every iSAFE deal in a systematic manner before being too entrenched in iSAFE deals.

iSAFE deals protect investors from liquidation and merger/acquisition events in case of which the iSAFE holders have equivalent rights as preferential stockholders. iSAFE holders are also sometimes offered a MFN (Most Favoured Nation) Clause and a Pro-Rata Rights clause. The MFN clause protects investors in case of a down round (where the company is valued lower than the valuation cap mentioned in the contract), while the Pro Rata Rights clause allows investors to buy additional common stock during the equity round, in proportion to the number of shares issued to the investor in the financing round during the conversion of the SAFE.

Delving into mathematics

In order to discern the real dilution percentage of the founders while issuing SAFE notes, let's walk through the following problem:

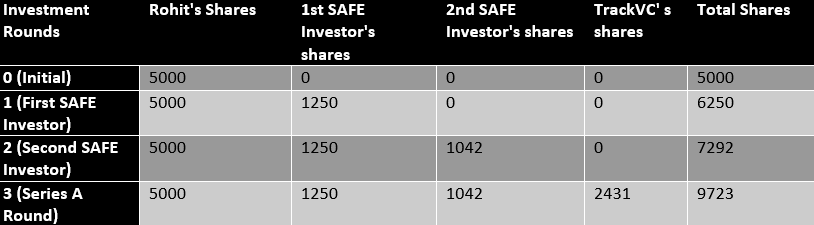

Consider a startup GrowNation whose founder Rohit Mehta raised the first $1 Million in pre-seed financing on SAFEs with a $5 Million post-money valuation cap. GrowNation seems to be a profitable venture, and thus caught the eye of angel investors who are willing to raise $1 Million via SAFE notes with a post-money valuation of $7 Million. Two years down the lane, GrowNation witnesses its Series A round, with TrackVC investing $5 Million on a $20 Million post-money valuation.

Let's for the time being assume that Rohit had 5000 shares of GrowNation before raising any funding. Now, most naïve founders would believe that only 25% of the company has been diluted (since they would only be referring to the Series A round and ignoring the SAFE rounds because the SAFE rounds won't be reflected in the static cap table which most founders are familiar with). Therefore, let's contruct a dynamic valuation cap table, taking into account each round of investments.

From an intutional analysis, you may have already deduced that at each step, the number of shares of a particular investor is equal to the amount invested by that shareholder divided by the pre-money valuation multiplied by the total number of shares before the investment. So for instance, in the first round, the amount invested is $1 Million, the pre-money valuation is $4 Million (Post-Money Valuation Cap minus the Amount invested) and the existing number of shares (before the investment) is 5000. Thus, total number of shares for the first SAFE investor is 1/4th of 5000 i.e. 1250. Although, it must be noted that the shares of the SAFE investors materialize only when the equity financing rounds occur.

This approach can assist the founder in deducing that the equity percentage of the founder has been diluted down to 5000/9723 i.e. 51.4%, compared to 75% which he was expecting.

Conclusion

iSAFEs (and other innovative financing mechanisms) are bound to grow in the future, since the traditional debt financing methodology of securing loans from banks has been rendered moot after the enactment of the Insolvency and Bankruptcy Code (2016). Various profitable startups such as BigBasket, Ola, BlacBuck and LendingKart have turned to debt financing from venture capitalists, with Trifecta Capital, Stride Ventures, Innoven Capital and Alteria Capital being the major players in the debt financing market. iSAFE thus presents a novel avenue for venture capitalists to mitigate risk, while also helping founders to raise funding without traversing through a plethora of legalities. But, the usage of iSAFE notes will be fruitful to the founders (and the firm) only if each of their clauses is clearly understood along with underlying implications on the financial scenario of the firm.

Each of the deals must be scrutinised before signing, and it entirely depends on the founders as to which method to pick to kickstart their high-growth venture and translate it into a profitable firm.

{kind=link}

{kind=link}