Investments: Do you need them?

When I was a kid, my dad explained how necessary it was to build a house with several pillars or columns. This was a vital element of any structure, which could help the house withstand any catastrophe. But do we construct a house with just one pillar? How many loads can that one pillar take? What will happen if it is not able to survive an earthquake?

While planning to buy or construct a house, we analyse everything in detail - the columns' size, their distancing and alignment, and so forth. Similarly, why should you not analyse your current financial situation in particular? Having a secured job is financial security, but having a recurring income source through non-formal sources, enough to meet your monthly expenditure is financial independence. Working forty-five hours a week to earn your income isn't as enjoyable as sleeping comfortably in your bed and receiving money in your bank account. Yes, this is possible. You have to put your money to the proper use.

"If you don't find a way to make money while you sleep, you will work until you die". — Warren Buffett

An increase in your Capital opens doors to new streams of income which, in turn, increase your savings. To harness the power of wealth creation, the only thing you need to do is invest your money in buying tangible assets. Investing possesses the ability to provide you with inflation-beating returns and enable you to harness passive income benefits. It would help if you started focusing on investing proactively by buying True Assets. Otherwise, all your efforts will result in just beating inflation, and not creating wealth, or enhancing your Capital.

What are True Assets?

In the last article, we talked about how true assets affect your life and your Capital. But what kind of investment options are we talking about? Traditionally, people used to invest in gold, silver, and land to save their money from inflation. They do provide satisfactory returns and are still preferred by many.

Real Estate

If you buy a house, the value will most probably increase with time; also, rents can be a great source of passive income. If we talked about the risks involved, there is a slight chance of reducing assets’ value. There are two significant problems with real estate investment. First of all, you need to invest a few lakhs. So you cannot utilize your small savings. Secondly, liquidity is low since it may take months to find a buyer at the right price. Despite all this, though, you can classify real estate investment as your True Asset.

Home: An asset or a liability?

Buying a home is often considered a milestone in our lives. A home is a dream for many while a necessity for all. How would you classify your house? Is it a true Asset? Ignore your emotions for some time and think from the sheer financial perspective you gained from this series.

One would always consider buying land as an investment and would see land as a True Asset. Historically, land has provided substantial returns to its investors.

Other forms of actual Assets:

When it comes to metals like gold and silver, they have been the most trusted form of investment in India, though they come with shortage, as theft is a significant risk. Gold has been successful in providing moderate returns, and its liquidity is also relatively high. But we think one should avoid investing in gold via jewelry, as making charges and other associated costs can bring down your return. In our opinion, the best way to invest in gold is through sovereign gold bonds issued by the RBI, where you don't have to be worried about storage costs or theft. Yet, you can take advantage of the appreciation of metal.

"How many millionaires do you know who have become wealthy by investing in savings accounts? I rest my case." — Robert G. Allen

Fixed deposits are another traditional form of True Asset, but they cannot generate spectacular returns.

Unveiling Equity Investment:

Do you ever dream of owning a business but hesitate due to lack of expertise, funds, and time? Well, in that case, one brilliant form of investment can be equity shares, where you can directly invest in any of the companies listed on the stock exchange. Investment in equity shares can be used to mobilize savings as low as Rs100, with the potential of growing them multiple times. Do you know that an investment of ₹ 10,000 in Infosys in 1993 would have grown to 400,00,000 by 2020? That's a 4000 times growth.

Another form of investment is Mutual Funds. A mutual fund is like an investment vehicle that invests in underlying assets such as stocks, bonds, other mutual funds, or any other asset. In this fund, you indirectly invest in all the companies that the fund has invested in. They are preferred for their liquidity and are perfect for mobilizing your small monthly savings, with the potential to provide inflation-beating returns.

Criteria for making investment choices:

You need to select the right investment instrument for yourself based on your investment amount, risk tolerance, returns required, and goals. Remember, don't put all your eggs in one basket. Diversify your investments using various instruments.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” – Phillip Fisher

The amount of risk that one should take should reduce with age. Thus, as you get older, we suggest that you should minimize your equity investments. As a thumb rule, subtract your age from 100, and that should be your maximum equity allocation. This means if you are 20, you can invest a maximum of 80 percent of your corpus in equity markets. If you consider putting all your money in real estate, read about the U.S housing bubble leading to a crash in the market. If you think FDs are the safest option, don't forget that their post-tax returns might not beat inflation. Similarly, stock markets and Mutual Funds are subjected to market risks. We suggest that you should invest in a properly balanced portfolio consisting of different investment instruments.

Mutual Funds

The first thing that would probably come to your mind in the case of Mutual Funds is the oft-repeated disclaimer, 'Mutual Funds are subjected to market risk. Read all scheme related documents carefully,' And they are usually promoted as 'Mutual Funds Sahi hai.' They possess the maximum potential to impact your Capital positively, do I say so? Let's explore…..

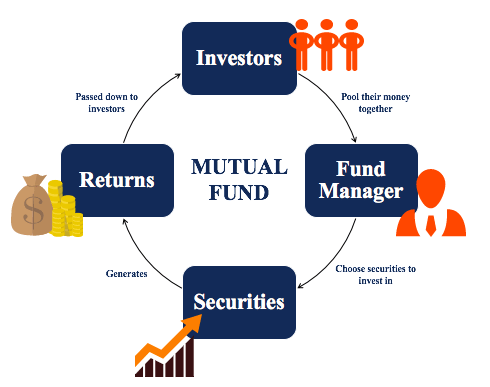

As the term suggests, Mutual Fund is a collection of funds mutually contributed by investors for a common purpose. Generally, the money collected is invested in various instruments such as stocks, bonds, gold, and other similar assets. These funds are operated and managed by fund managers, who control the underlying investments in such a manner as to produce maximum gains.

But how are mutual funds and stock markets related?

Warren Buffett has advised that one should never put all one's eggs in one basket. We cannot be sure about any company's future. It can be a company like Kingfisher Airlines, which went bankrupt. It can be like Reliance Industries, which has been able to give manifold returns. Therefore, you must diversify by investing in various companies. But again, what if all your selected stocks are not performing well? Don't worry; there is a solution to every problem. Suppose you do not have enough knowledge about markets' functioning or do not have time to do proper research. In that case, you can easily rely on Mutual Funds. In Mutual Funds, a fund manager makes all decisions for you regarding which instrument to buy and other such intermediate choices at a nominal fee. All you have to do is purchase Mutual units funds based on your investment objectives and time horizon.

"Equity mutual funds are the perfect solution for people who want to own stocks without doing their own research" – Peter Lynch

Why Mutual Funds:

1. Diversification:

You can quickly diversify your portfolio as there are Mutual Funds for a variety of assets. This helps in reducing risk too a great extent.

2. Liquidity:

They can be redeemed easily. Whenever you need the funds, you can submit a redemption request, and you can receive the funds in your bank account within one to three days.

3. Economies of Scale:

Creating a diverse portfolio requires many transactions. For each type of instrument you want to invest in, you need to make a separate transaction. There is a fee associated with each transaction that will add up to huge costs; mutual funds solve this problem because they buy and sell large quantities of securities, which reduces transaction costs.

4. Professional Management:

The most significant advantage of a Mutual Fund is the professional management by knowledgeable fund managers. They do all the research to identify potential multibagger stocks. The fund companies manage all administrative activities and compliances.

5. A variety of choices:

Different Mutual fund managers follow different styles and strategies to design an investment portfolio according to different goals. The strategy can be value, growth, low risk, and many others. You have the freedom to select any of these funds after proper research and evaluation.

Types of Mutual Funds

1. Equity - Oriented Mutual Funds

As the name suggests, equity-oriented Mutual Funds invest their funds predominantly in equity shares of companies. Generally, investments are made in companies from different sectors. This diversification is done to reduce the risk associated with market fluctuations. If you are looking to invest for a more extended period, then you should go ahead.

Equity funds can be further classified as:

a) Large Cap Funds

b) Mid-cap funds

c) Small-cap funds

d) Sector funds

e) Index funds

f) Exchange-traded funds

g) ELSS funds

2. Debt Funds:

Debt funds invest in the debt securities issued by corporates and the government. These include bonds, debentures, and commercial papers. Such funds are ideal for risk-averse investors, who are satisfied with lower but fixed returns. Debt funds can be classified based on security and time horizon as follows:

a) Overnight funds

b) Ultra-Short duration funds

c) Low duration funds

d) Short duration funds

e) Money market funds

f) Liquid funds

g) Gilt funds

h) Corporate bond funds

3. Balanced or Hybrid funds:

Mutual funds with debt and equity instruments in different proportions are called hybrid funds. The objective behind such funds is to diversify your portfolio and reduce exposure to market risks by investing in varied assets. These funds are suitable for moderate risk appetite investors.

4. Other funds :

- Emerging market fund

- Fund of funds

- International fund

- Gold mutual funds

- Real estate funds and many more

OUR OPINION:

Debt Funds are not entirely risk-free, especially since defaults have been a problem for the last few years. Balanced fund managers charge a higher fee for these funds compared to the returns they provide. Fund houses generally charge a higher management fee for Equity funds due to the work's complexity. ICICI Balanced Fund has invested almost half its funds in debt instruments, and the fee charged is almost equal to that of Equity Fund. Also, currently, the taxes on long-term capital gains on equity-oriented Mutual Funds are way less than that of Debt funds. Thus we feel Equity Funds will provide better post-tax returns when compared to debt or balanced funds. Generally, equity markets offer a compounded growth rate of 10-12%. This means that even if you stay invested in Index Funds, you could conveniently grow your money at an average rate of 10%. However, equity-oriented Mutual Funds provide returns ranging from 12% to 18% on investment.

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” – Albert Einstein

How can you invest in Mutual Funds?

There are two major ways of investing in any Mutual Fund- systematic investment plan(SIP) and lump-sum investment. If you opt for SIP, you can invest small amounts at regular intervals, such as monthly or quarterly. The investment amount will be directly deducted from your bank account, so you don’t have to go through the trouble of making the payment every time. On, the other hand, investing in a lump sum means making a one-time bulk investment. Even, if you are investing a lump sum, the minimum investment amount can be as low as ₹1000.

In our opinion, SIP is a great option to invest in regularly. Since the amount gets automatically deducted, investors do not bother altering the procedure and end up creating substantial Personal Capital for themselves. Investing via SIPs averages out the fluctuations in purchase price due to market up-downs. A lump sum investment can also opt for if you have received a substantial one-time amount. But, prefer making a lump-sum investment in Mutual Fund only after analyzing the market thoroughly, so you don’t end up buying the units at an expensive price.

Parameters to consider before buying funds:

- Risk Profile - If you are risk-seeking then you consider small-cap funds, while if you are risk-averse then go for large-cap funds

- Asset Under Management - If you are opting for small-cap or mid-cap funds, look for funds with lower AUM; in all other cases, the higher the AUM, the better it is

- Expense Ratio - A higher expense ratio will reduce your return. It should be as low as possible

- Portfolio Turnover Ratio- Always compare PTR with returns. A higher PTR is justified with high returns

- Exit load - This is the fee charged by the fund house if investors redeem their units before a specified period. Always factor in the exit load before taking a decision.

Finally, always remember that past returns are no indication of what will happen in the future. You need to evaluate what changes are likely to occur that will impact the performance of different categories and kinds of mutual funds and other investment avenues.

With this, give yourself a pat on the back, for making this so far to the end of this lengthy write-up. You have definitely got closer to your aim to achieve financial independence. We hoped that you have gained substantial knowledge on investment.

Happy investing!