Introduction

Let's start with the bitter and stark truth of life - the importance of money. If life for you is just about fulfilling your basic needs, maybe you have reached the zenith of spirituality. You would have indeed thought to yourself at some point in life, ' If I had enough money.....' It's funny that nobody knows what ' enough ' actually is. Now when you are not sure of the amount you wish to have, what happens, as a result, is that financial planning becomes subjective and is neglected because planning requires a destination. This is where you need ' personal finance management ' to come into the picture. Sadly the subject of personal money management is not taught in the regular academic curriculum. To cover this, we will run a series of articles that will prevent you from making lousy money mistakes. Reading this will help you improve your financial decision-making and take small steps in life that can make a substantial positive difference later on.

Wealth Creation

Saving: The ignored "Financial Angel"

Saving is the first step towards ‘Minting your Money.’ Saving money can be compared to charity. Everyone knows and agrees it’s good, but few do it. On asked about savings, we give reasons like ‘ Mehangai Kafi badh Gayi hai,’ ‘One should live in the present and not think much about the future and so on. So, the question is, how can we save more money? It’s never about the amount but the way we spend. Just think it over. Let’s understand it mathematically:

Savings = Income - Expenditure

Savings depend not only on your income but on your expenditure too. At any point in time, you can boost your savings by planning your expenditure well. Conversely, you may not affect your savings even after increasing monthly income if expenditure also increases.

This brings me to an interesting quote by Warren Buffet, “Do not save what is left after spending, but spend what is left after saving.”

I believe saving is like a healthy meal which should be consumed regularly to have a financially healthy life.

Transform your Savings into Personal Capital:

People often misunderstand their saving as personal capital. Saving is that part of your monthly cheque that you choose not to spend. You might be saving it to spend it in the next big billion days or a great Indian sale, but you are saving it for now. If you channelize your savings correctly, they can only be treated as the first step towards building your capital. If you are stuck in the cycle of saving money to spend more, you will never be able to convert it into personal capital. Millionaires accumulate wealth not just by earning vast amounts but by not spending the money they make- and instead investing it.

Budgeting: As Simple as it Can Be

Many people are simply afraid of the term “budgeting.” But budgeting is not as complicated as it sounds. I am not asking you to start preparing balance sheets and indulge in financial modeling. Budgeting is nothing but managing your expenses, that is, allocating portions of your income for individual purposes or essentials and not spending more than the specified limits.

Budgeting has only one rule: Do not go over budget.” ― Leslie Tayne

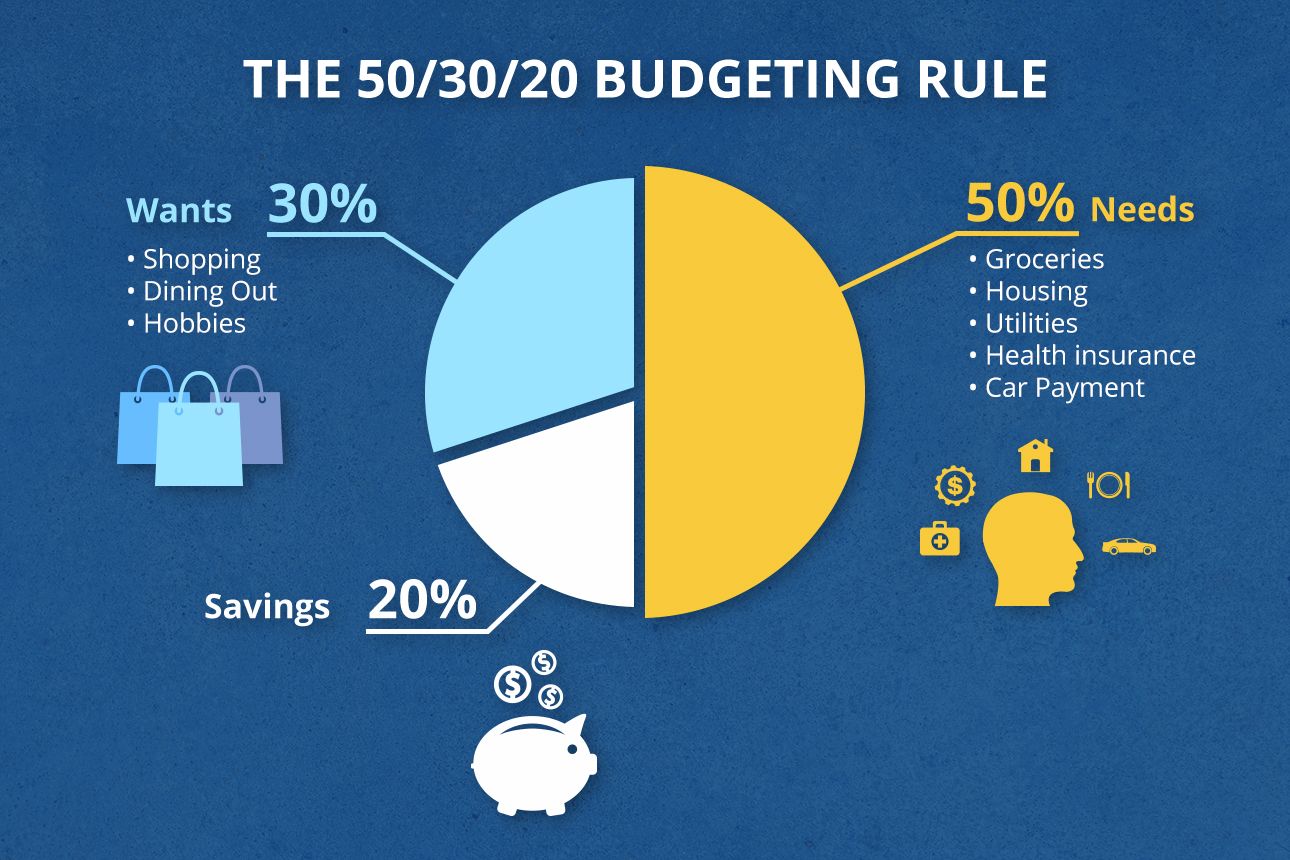

This brings me to the famous 50-30-20 rule. The rule says you should spend a maximum of 50 % of your monthly earnings on essentials such as food and shelter, not more than thirty percent on wants and luxuries, and save at least 20% for your future. Following it diligently in your monthly budgeting will introduce some financial discipline in your life. The rule doesn’t stop you from spending on fancy dinners and lavish parties but limiting your expenses. This will help you to avoid overspending and save more. Giving labels to your money will help control your cravings and prevent irresponsible spending.

Know your Budget :

You cannot budget properly if you don’t know what your budget is made up of. Two significant components of your budget are static budget and flexible budget. A fixed budget consists of values that are fixed and do not change throughout the budget period. A flexible budget includes items that are not constant, such as clothing, travel, outings, festival expenses, etc. The static part of a budget makes you aware of your fixed payments, and after considering the flexible ones, you can forecast your costs. By doing the mentioned activity, you can quickly identify the months of high and low expenses and prepare a financial plan accordingly to achieve goals. You can save money for a vacation, a new vehicle, a new home, a retirement fund, or any other investments.

“Money, like emotions, is something you must control to keep your life on the right track.” - Natasha Munson

How to create a budget:

A budget should be based on individual financial goals. However, it is recommended to follow the following sequence of goals:

Create an emergency fund

Settle your debt

Create or enhance personal finance

The standard checklist you need to remember :

- Create a list of all your income or cash inflows

- List all expenses or cash outflows

- Allocate suitable money to each of your essential expenses

- Start allocating money for an emergency fund

- Set goals with time horizons and allocate some portion of earning towards them

- Track your spending regularly

- Check what costs you cut down and what you can do to increase your cash inflows.

Smart ways to save more:

With savings, emergency funds, and proper budgeting, you can live a financially healthy life. But we can permanently save more by slightly improving our lifestyle or by slightly changing our habits.

- Stop using Credit cards.

If you are using credit cards, you might end up making impulse purchases—the willingness to pay increases with a credit card. So, if you pay for things with plastic, you tend to spend more when you pay with cash.

2. Keep your emergency fund in a separate bank account

This will ensure that you don’t lose money to impulsive purchases, mistakes, or oversight. However, at the time of emergencies, you can quickly write yourself a cheque.

3. Sell unnecessary ITEMS

This will bring in some money, save space and allow you to analyze your past spending habits. Don’t think of it as a harmful activity; instead, enjoy the process.

4. Cancel your unnecessary subscriptions

With our changing lifestyle and needs, we must be mindful of your subscriptions. Perhaps we don’t require a particular service anymore.

5. Avoid Impulse Purchases

The primary reason behind extra spending is impulse purchases, and most of the time, we end up buying unnecessary items just because of our mood or impressive marketing. Give yourself ample time and think before purchase.

Finally, as they say, ‘You can take a horse to water, but you can’t make it drink. Similarly, whatever I have presented, it is finally your decision to save and enhance your capital or keep spending on and on…….